Buying your very first residence is a captivating – as well as daunting – techniques. An advance payment to the a new residence is always a first-go out consumer’s biggest financial investment yet, and in many cases they want to imagine all of their choices for investing it – also having fun with 401(k) advancing years financing.

But can you really use your 401(k) to fund a home? Whenever its invited, should you take action?

The reality is that it is some a complex matter. Throughout the sections you to follow, we are going to walk you through it to pay for:

- Whether 401(k) money can be put on a property (spoiler: yes)

- Choices for delivering funds from their 401(k) membership

- Pros and cons of using 401(k) money to make a down-payment on the home

- The way it stands up some other old-fashioned financial options

Short Takeaways

- Customers can access money from the 401(k) thanks to a loan or an outright detachment.

- Downright withdrawals of 401(k) financing bear significant punishment and you can tax expenses.

- First-day home buyers will consider using 401(k) funds to shop for a property when they do not have enough discounts to have a traditional downpayment.

- Very financial specialists suggest facing using 401(k) money to fund a home.

- Discover flexible financial choices (for example FHA or any other first-go out consumer software) that enable people to pick residential property which have very low advance payment requirements.

The fresh new brief address: sure. You need the 401(k) making a down-payment in your basic family. While you are 401(k)s are designed especially so you’re able to prompt preserving having retirement, it is your finances, and you can log in to anytime.

401(k) Financing

Really 401(k) package team wanted you to borrowers spend the money for financing straight back in this five many years. You’ll also have to pay the loan back which have attention, while the visible work for is you pays it right back in order to oneself.

Supposed the mortgage route may also steer clear of the 10% very early withdrawal penalty (given to anyone who withdraws fund in advance of decades 59?). In addition it won’t effect your credit report otherwise your debt-to-earnings ratio, one another tall gurus if you have reasonable borrowing from the bank otherwise who don’t require its credit inspired with other explanations.

The absolute most you could potentially borrow from the 401(k) are $50,000 otherwise half your current vested interest (any sort of is gloomier) browse around this web-site.

Although this could possibly get every sound ideal, there are many cons. Taking right out that loan out of your 401(k) typically freezes brand new account – you simply can’t create most benefits in lifetime of your loan, and you may employers can not lead, both. As you spend the loan straight back, you are able to overlook gains opportunities for the old-age money.

Additional drawback would be the fact adopting the four-12 months identity, unpaid money are thought an outright withdrawal, and this incurs taxation or other economic punishment.

401(k) Detachment

One other (faster trendy) option is to take an outright withdrawal from the 401(k) funds. Why it’s such as for example an undesirable choice is which you’ll automatically pay an effective 10% penalty on the financing your withdraw and you will shell out taxation at the top of it. That said, you don’t need to pay back the cash your withdraw. In certain facts, some body may suffer that work with outweighs others economic penalties incurred.

There is zero restriction into the number you might withdraw away from your account. You could potentially take-out as much money as you want once the much time since it is equivalent otherwise lower than your vested interest.

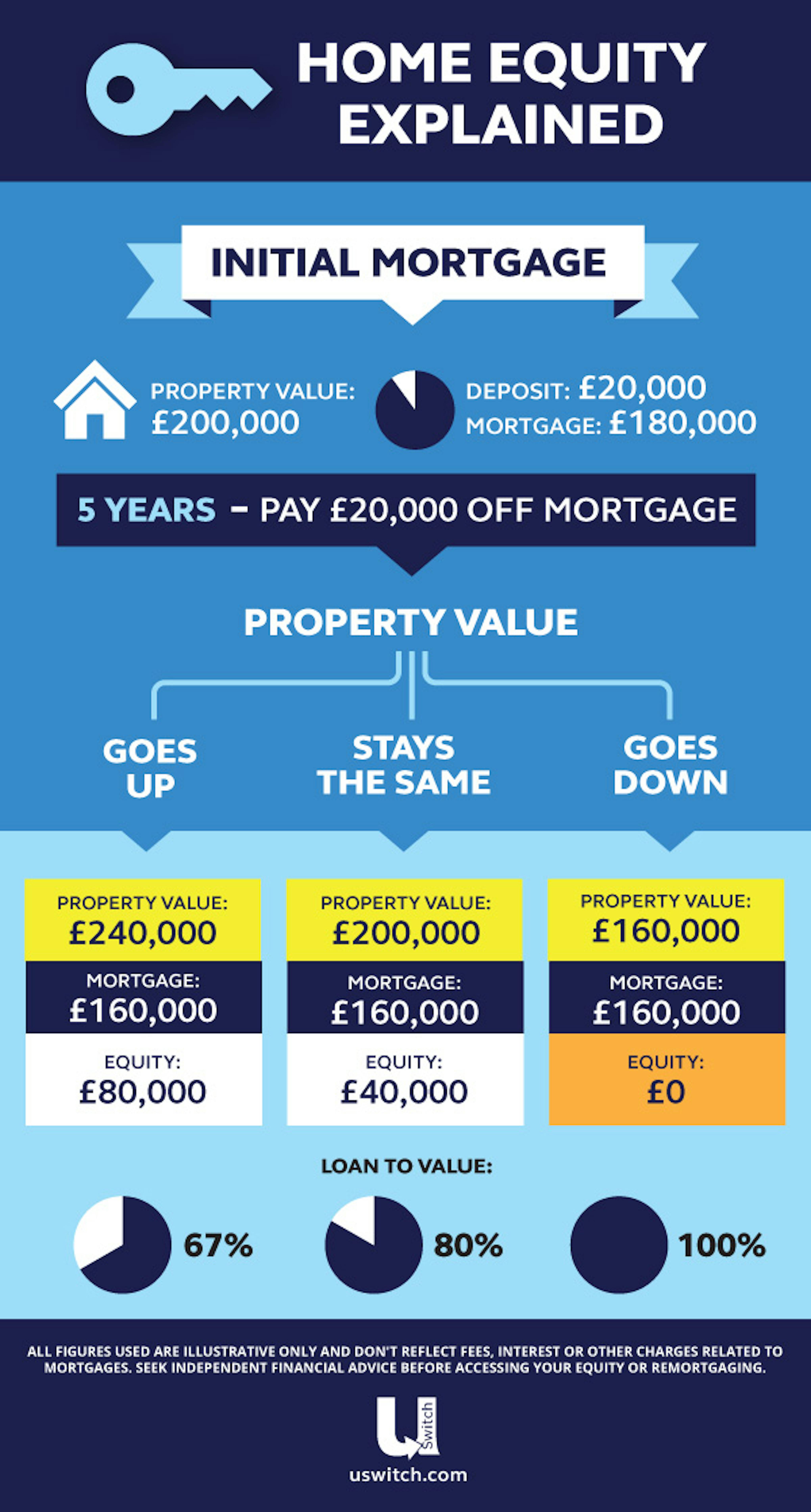

On the example lower than, you can find the difference between taking right out an excellent 401(k) financing versus. a total detachment from a merchant account that have an initial harmony out of $38,000.

There are numerous reasons a first time domestic client will get thought having fun with 401(k) loans to fund another domestic. Generally, it is completed to meet an instant cash you would like to help you make down payment into the a home – as an instance, whenever a first-time home buyer does not have any discounts to have an advance payment however, would like to benefit from reduced mortgage interest rates.

Homebuyers would be keen on the low interest rate with the 401(k) finance vs. most other down payment mortgage choice. Of numerous first-time homebuyers are also younger, so a bump on the senior years savings may not feel just like such an issue.

But the truth is you to definitely even if you may be younger, deleting money from retirement account can be rather hurt the growth possible minimizing the total amount you can save for old age when you look at the the end.

Whichever economic mentor will say to you it shouldn’t end up being your first choice, and some will tell you to not ever take action around any items.

Because the you have gathered, the newest brief solution to it question is zero. Whether you decide to sign up for a good 401(k) loan otherwise outright detachment, discover bad economic consequences in the way of often punishment repaid or shed development in your retirement money.

A far greater option is to take advantage of first-time homebuyer programs offering low-down commission applications as well as down-payment advice sometimes. We have curated a summary of very first-day homebuyer applications in Ohio in this article. If you’re an additional state, an easy Google getting first time domestic visitors software along with your condition provides you with a listing of a beneficial solutions.

There are even standard domestic consumer mortgage software such as for instance FHA you to only require an effective step 3.5% off and are will recognized if you have smaller-than-stellar credit ratings. Lower than are a complete self-help guide to 2022 FHA criteria:

The greatest Takeaway

First time homeowners may use its 401(k)s to purchase a home, there try actually glamorous positive points to performing this. Although best financial decision is to leave your 401(k) having advancing years.

As an alternative, consider other monetary possibilities designed for real estate that present equivalent (if not more) autonomy and comfort.

Trying to find a house near Dayton?

If you’re relocating to the Dayton urban area, the team on Oberer Residential property helps you come across (otherwise make!) your ideal home. Contact us right now to begin!